Cement industry in Vietnam facing

big surplus capacities

![17 Project development up to 2013 (OneStone [1])](https://www.zkg-online.info/imgs/101523213_cc71b9db11.jpg)

Summary: In recent years, no other country in South East Asia has experienced such dynamic development as Vietnam. Its economic growth is only slightly lower than those of China and India. Since 2001, the average annual growth in cement consumption has been approx. 12.5 %. Vietnam managed this rate of growth without resorting to a high rate of importation. This feat was achieved by a cement industry that had been in a state of devastation in 1975, the year in which North and South Vietnam were reunited. In 2010, cement production capacity is set to reach a figure of 78 million t/a. This means that Vietnam will possess significantly more capacity than actually necessary for covering its own requirements. This report describes the consequences of this situation and outlines the overall development of the cement industry.

Since the last decade, Vietnam has been one of the fastest growing economies in the world. A spirit of great commitment is to be felt everywhere in the country, as well as hope for a better future. The country has also come through the global economic crisis surprisingly well. It had an economic growth of 5.3 % in 2009, which is only marginally lower than the previous year’s figure of 6.2 %. Particularly at the end of 2009 there was a clear upturn in economic growth, with 6.0 % in the 3rd quarter and 6.9 % in the 4th quarter. To stimulate the economy, the government...

Since the last decade, Vietnam has been one of the fastest growing economies in the world. A spirit of great commitment is to be felt everywhere in the country, as well as hope for a better future. The country has also come through the global economic crisis surprisingly well. It had an economic growth of 5.3 % in 2009, which is only marginally lower than the previous year’s figure of 6.2 %. Particularly at the end of 2009 there was a clear upturn in economic growth, with 6.0 % in the 3rd quarter and 6.9 % in the 4th quarter. To stimulate the economy, the government earmarked 17 trillion Dong (9.2 billion US$) for an interest subsidy of 4 %. This led to an increase in investments but also raised bank credit grants by almost 38 %, after the already steep increase of 25 % in the previous year.

An economic growth of 7.0 to 7.5 % is forecast for 2010. Goldman Sachs even sees the possibility that growth could reach 8.2 %. However, economic development will be strongly dependent on Vietnamese fiscal policy and on developments as regards credit grants, inflation and the trade balance deficit. Although the inflation rate declined from 23 % to around 7 % in recent years, a rise to over 10 % is feared for 2010. This could mean that, following the devaluation by 5 % in 2009, the Vietnamese currency may suffer a further loss in value against the US Dollar. Although this could lead to an increase in exports, the 12.25 billion US$ trade balance deficit will hardly be reduced because the economy is dependent on expensive raw materials, machines and plants. Since joining the WTO in 2007, Vietnam has become the second largest exporter of rice, but the overall export economy is not expected to grow by more than 7 %.

The fact that over 60 % of its population are employed in the rural economy shows that Vietnam is still largely an agricultural country. However, agriculture only contributed 20.7 % of the economic performance in 2009. The service sector was responsible for 39.1 % and the industrial and construction sectors brought in 40.2 %. In 2009, the construction economy experienced a growth rate of 11.4 %, making it the driving force behind the economic growth. It profited from cheap credits and after a period of stagnation in the preceding year, large investments for housing and commercial construction were again undertaken. In Vietnam there is a lack of retail property and housing, especially in the growing cities in the north and south of the country. Apartments for people in the lower and medium income groups have proved to be the motor of construction activity. However, in view of the rapid economic development the entire infrastructure of the country has become overloaded and is in urgent need of investment.

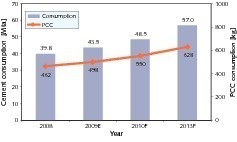

Vietnam’s cement industry has developed at a breathtaking pace in recent years. Coming from a cement consumption figure of 16.7 million tonnes per year (Mta) in 2001, consumption in 2009 reached an estimated 43.5 Mta, which corresponds to an average annual growth rate of 12.5 % [1]. Figure 1 shows the development of cement consumption and per-capita consumption as from 2008 with an estimate of developments until 2013. In 2008 the cement consumption was 39.8 Mta and for 2010 an increase to 48.5 Mta is expected, which corresponds to annual rates of increase of 9.3 % in 2009 and 11.5 % in 2010. However, after that only small rates of growth are anticipated due to impending saturation, a consumption figure of 57 Mta is forecast for 2013. On that basis, the per-capita consumption of 462 kg in 2008 will rise to approx. 550 kg in 2010 and 628 kg in 2013.

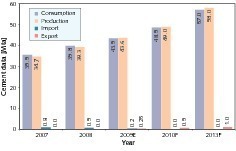

Figure 2 presents the development of cement consumption, production, imports and exports. Cement production and consumption are at approximately the same level. The lower production rates from 2007 to 2009 are compensated by imports, mainly from China. Among the countries hitherto receiving exports from Vietnam are Laos, Cambodia and Mozambique, although exports have not so far played any significant role. In 2009 the export figure of 0.25 Mta is for the first time higher than the import rate of 0.2 Mta. Theoretically, the country could do without imports after 2009. Exports from Vietnam will then essentially be regulated by the country’s international competitiveness and the requirements of the most important purchasing countries. Due to the relatively high costs of grinding in comparison to other countries in the region, it is likely that clinker exports will assume greater importance than cement exports. Until 2009, Vietnam was still dependent on clinker imports from China and Thailand.

One important factor for the increase in cement sales was the decision to use concrete instead of asphalt as from April 2009 for highway projects. Also, cement prices dropped by about 5 % due to increased competition, which provided a further boost for cement sales. However, cement factory locations by no means blanket the country. This is due to the fact that raw material deposits, and therefore most of the integrated cement plants, are predominantly to be found in the north of Vietnam. In central and south Vietnam there are only a few raw material deposits and cement factories, but numerous grinding plants. The total number of pure grinding plants is stated to be 30, but only about 17 of these (status 2009) have a capacity > 0.1 Mta. Approximately 12.5 Mta of cement were transported from the north of country to supply southern Vietnamese markets in 2009.

In 2009, Vietnam possessed 105 kiln plants with a production capacity of 61 Mta. However, this figure of over 100 kiln plants includes 55 shaft kiln plants with a capacity of approx. 5.0 Mta, most of which were built in the 1990s. More than half the shaft kilns have a capacity of less than 0.05 Mta, with 17 having a capacity below 0.02 Mta. The majority of these plants are located in the north of Vietnam. They are insignificant for the future development of the industry, firstly because their high energy consumption makes them far too expensive to operate and secondly because the total cement output rate of shaft kiln plants is estimated to be not more than 2.7 Mta. It is therefore logical that numerous shaft kilns will be shut down in coming years.

Vietnam’s cement industry can be divided into three groups – state-owned companies, joint ventures and other companies, which include the owners of the shaft kiln plants. Table 1 provides an overview of the leading companies in 2009. There are 33 integrated cement plants (excluding shaft kiln plants) and 17 grinding plants with capacities exceeding 0.1 Mta. The country’s total cement production capacity including shaft kiln plants is 61 Mta, which at a production rate of 49.3 Mta corresponds to a capacity utilization of 71.5 %. However, when considering these figures it must be remembered that they include shaft kilns with a still lower degree of utilization and that, because of the numerous separate grinding plants in central and southern Vietnam, no particularly high utilization of the cement production capacity can be achieved.

The most important company with a share of around 34 % in the country’s cement production capacity and an estimated 37 % in actual cement output is the state-owned Vicem (formerly Vietnam National Cement Corporation or VNCC). Vicem owns a total of nine integrated cement plants and a number of grinding plants. Although VNCC was established as recently as 1994, Vietnam had one of the first cement factories in Asia with Hai Phong Cement, which went into production in 1889. In 1975, the year of the country’s reunification, the cement industry was in a desolate state. The first step in its reconstruction was Bim Son Cement’s new 1.2 Mta line, commissioned in 1981, with two wet-process kilns and Russian technology. The first dry-process kiln was constructed in 1983 by FLSmidth for Hoang Thach Cement (Fig. 3). Today, Hoang Thach Cement is one of Vicem’s largest plants, with a production capacity of 3.5 Mta and three modern lines.

With Hoang Thach, Hai Phong, Bim Son, But Son, Hoang Mai, Tam Diep (formerly Ninh Binh Cement) and Hai Van, Vicem owns seven factories in northern Vietnam. Hai Phong Cement (Fig. 4) has a capacity of 3.0 Mta with its two 1.4 Mta capacity lines and a 0.2 Mta white cement line. Hoang Mai Cement (Fig. 5) with its capacity of 1.4 Mta is one of the plants that so far only have one production line. In southern Vietnam, Vicem operates the Ha Tien1 and Ha Tien 2 factories as well as several grinding plants. Ha Tien 1, located at Binh Phuoc (Fig. 6) has recently commissioned a second plant with a capacity of 2.0 Mta. Ha Tien 2, located in the Kien Giang province, at the southernmost point in Vietnam, close to the Cambodian border, has a production capacity of 1.9 Mta of clinker and 0.9 Mta of cement. Most of the clinker produced is ground in one of the grinding plants in Ho Chi Minh City or in Long An province.

Joint venture (JV) enterprises have a 30 % share in the country’s cement production capacity. These are JV with Vicem and JV with other cement producers in Vietnam. The No. 1 JV is Holcim Vietnam, with its cement production capacity of 4.7 Mta from one integrated plant and three grinding plants. Holcim entered the market in 1996 with Hong Chong Cement (formerly Morning Star), which is also located in Kien Giang Province. Vicem has a 65 % holding in Holcim Vietnam, while 35 % is held by Ha Tien 1. At an early stage, Holcim decided on a concept based on cement terminals and separate grinding plants. Holcim’s Terminals (Fig. 7), like many others in Vietnam, distribute its cement by ship. The Cat Lai grinding plant has a capacity of 1.8 Mta and is in a strategically favourable location for supplying the markets of HCM City.

Nghi Son Cement a JV of Taiheiyo Cement and Mitsubishi Material (total holding 65 %) with VNCC (35 %) started producing in 2000. The plant (Fig. 8) is located in the northern province of Thanh Hoa. It has two 2.15 Mta production lines and two 1.5 Mta cement terminals in Hiep Phuoc and Ninh Thuy. Lucky Cement of Taiwan has a 90 % holding in Phuoc Son Cement. Hai Duong Cement holds the other 10 %. The company’s first 1.8 Mta plant (Fig. 9) was commissioned in 2005 and a second plant with the same capacity followed in 2009. The next place is taken by Chinfon Cement, in which the Taiwanese Chinfon Investment Co. holds 70 %, VNCC 14.44 % and Minh Duc Limestone Exploitation the remaining 15.56 %. The JV was founded in 1992. The plant (Fig. 10) is located near Hai Phong in northern Vietnam. With its two 1.6 Mta production lines and one 0.5 Mta grinding plant the company has a cement production capacity of 3.7 Mta. One of the other joint ventures is Lafarge Vietnam, which has a 70 % holding in a 0.5 Mta grinding plant.

The list of other cement producers, which have a total market share of 33 %, is headed by Cam Pha Cement and Thang Long Cement. Cam Pha Cement is one of Vietnam’s larger cement works with a 6000 t/d line (Fig. 11), constructed for Vinaconex. This cement works also operates a separate grinding plant. Thang Long, located in Quang Ninh province, is a cooperative venture of Geleximco and Lilama and has a modern 6000 t/d line (Fig. 12) with a cement production capacity of 2.3 Mta. For its raw material imports and cement exports the factory uses a deep water harbour for 30 000 dwt ships. It also operates a 1.2 Mta grinding plant. The Ha Long Joint Stock Company (HLCC) is No. 8 in the TOP 10, having a capacity of 2.5 Mta. Luks Cement (Vietnam) is the No. 9 operating a cement factory with two lines in the old imperial city of Hue, as well as a separate grinding plant, with a total capacity of 2.1 Mta.

Cosevco Cement, with its 4000 t/d clinker production line in Song Gianh (Fig. 13) is a member company of the Midland Construction Corporation. Cosevco is one of Vietnam’s leading construction companies [2]. Its other activities are in the tile manufacturing sector. Vinaincon, acting as general contractor, built the 4000 t/d Quang Son plant (Fig. 14) using French technology. This plant is situated in Thai Nguyen province, about 100 km north of Ha Noi, and was constructed on a green field site, like so many new cement factories in Vietnam. It uses anthracite as fuel, which is typical for numerous Vietnamese plants. As at the Cam Pha grinding plant, Horomill horizontal mills are used for the cement grinding. Another large cement manufacturer is TAFICO (FICO TayNinh Joint Stock Company), which operates a 4000 t/d plant (Fig. 15) in Tay Ninh province.

Vinakansai Cement and the Quang Ninh Construction and Cement Joint Stock Company (QNCC), whose plants include Lam Thach Cement, are also among the cement manufacturers that operate more than one production line. In addition to these, there are a number of cement plants with capacities of 1 Mta or less. The typical 1 Mta or 2500–3000 t/d plants were constructed by Chinese EPC contractors. One example is Song Thao Cement (Fig. 16), commissioned in 2009, while another is Hoa Phat Cement. The list of further manufacturers includes Kien Giang Cement Joint Stock Company, DIC Binh Duong Cement, Buu Long Cotex Invest & Industry and about 45 companies operating shaft kiln plants.

In a recent study 39 cement plant projects with planned commissioning dates in the period 2009 to 2012 were identified [1]. The production capacity of these projects totals approx. 55 Mta. Figure 17 presents an overview of the cement projects up to 2013 according to the actual project planning and according to the OneStone forecast. OneStone established that only 13.2 Mta of new capacity went into operation in 2009, because various projects had to be postponed and other projects were not completed on schedule in that year. Among the plants actually completed are Binh Phuoc (2.0 Mta), Hoang Thach 3 (1.2), But Son 2 (1.4), Ha Long Grinding (1.25), Thang Long Cement (2.3), Dien Bien Cement (0.4), Xining Cement (1.5) Dong Son Cement (1.5) Quang Son Cement (1.5) and Song Thao Cement (1.0).

If all the projects contained in the OneStone forecast are really completed by 2013, Vietnam may then have a cement production capacity of 110 Mta. However, it is assumed that actual production capacity will only increase to 103 Mta, i. e. that approx. 7.0 Mta of existing capacity will have to be shut down. This will mainly affect shaft kiln plants and some wet-process lines and mini cement plants. Another aspect is that the Ministry of Construction already warned of surplus capacity in the cement industry at the beginning of 2009. Based on the assumption that a large surplus capacity will inevitably occur in the coming years due to existing plants and those already under construction, the ministry does not intend to grant any more licences during the next 10 years.

According to the ministry’s own forecast, a cement production capacity of 102 Mta, which is only slightly above the forecast consumption figure of 95 Mta, will not be reached until 2020. Cement producers, and particularly Vicem, have been called upon to concentrate more strongly on exports. However, some experts in the Vietnamese cement industry are questioning whether exportation at competitive prices will actually be possible. The first projects to fall victim to the ministry’s new decree were four cement plants in the northeast of the country planned by Huu Nghi and Yen Mao Cement in Phu Tho province, by Phu Tan Cement in Hai Duong province and by Ngoc Ha Cement in Ha Giang province. The ministry commented that all the above projects are small ones planned by local private companies. It also stated that it would not permit any further projects for plants with production capacities below 3000 t/d.

Following the cement industry’s many years of two-digit growth rates, it is expected that growth will slow down significantly in the coming years. At present, Vietnam is still classified as an agricultural economy. The clinker and cement production capacity available in 2010 is sufficient to meet the requirements of the whole country. Another approx. 45 Mta are going to come online between 2010 and 2013, although the Ministry of Construction has stated its intention to stop or restrict the granting of licences for new projects for the next decade. It would seem that at least no more new plants with clinker capacities below 3000 t/d will be built. The present capacity utilization of cement grinding systems is still above 70 %. By 2013 this will decline to around 55 % unless Vietnam manages to achieve significant export figures and shut down existing uneconomic capacity.

Überschrift Bezahlschranke (EN)

tab ZKG KOMBI EN

This is a trial offer for programming testing only. It does not entitle you to a valid subscription and is intended purely for testing purposes. Please do not follow this process.

This is a trial offer for programming testing only. It does not entitle you to a valid subscription and is intended purely for testing purposes. Please do not follow this process.

tab ZKG KOMBI Study test

This is a trial offer for programming testing only. It does not entitle you to a valid subscription and is intended purely for testing purposes. Please do not follow this process.

This is a trial offer for programming testing only. It does not entitle you to a valid subscription and is intended purely for testing purposes. Please do not follow this process.