ASEAN cement industry on the upswing

Source/Quelle: IMF

Source/Quelle: IMF

Source/Quelle: Harder

Source/Quelle: Harder

Source/Quelle: Asosiasi Semen Indonesia, OneStone

Source/Quelle: Asosiasi Semen Indonesia, OneStone

Source/Quelle: OneStone

Source/Quelle: OneStone

Source/Quelle: Semen Gresik

Source/Quelle: Semen Gresik

Source/Quelle: HeidelbergCement

Source/Quelle: HeidelbergCement

Source/Quelle: Holcim

Source/Quelle: Holcim

Source/Quelle: PT Semen Andanas

Source/Quelle: PT Semen Andanas

Source/Quelle: CNCA, OneStone

Source/Quelle: CNCA, OneStone

Source/Quelle: OneStone

Source/Quelle: OneStone

Source/Quelle: Lafarge

Source/Quelle: Lafarge

Source/Quelle: IBAU HAMBURG

Source/Quelle: IBAU HAMBURG

Source/Quelle: cemap, OneStone

Source/Quelle: cemap, OneStone

Source/Quelle: OneStone

Source/Quelle: OneStone

Source/Quelle: Holcim

Source/Quelle: Holcim

Source/Quelle: Lafarge

Source/Quelle: Lafarge

Source/Quelle: TCMA, OneStone

Source/Quelle: TCMA, OneStone

Source/Quelle: SCG, OneStone

Source/Quelle: SCG, OneStone

Source/Quelle: SCG

Source/Quelle: SCG

Source/Quelle: Holcim

Source/Quelle: Holcim

Source/Quelle:Italcementi

Source/Quelle:Italcementi

Source/Quelle: VNCA, OneStone

Source/Quelle: VNCA, OneStone

Source/Quelle: Ximang HaiPhong

Source/Quelle: Ximang HaiPhong

Source/Quelle: Vinaconex

Source/Quelle: Vinaconex

Summary: The ASEAN countries in Southeast Asia are currently one of the driving forces of the world economy, experiencing an economic growth of between 6 and 15%. Economic stimulus packages introduced by the governments of the region have resulted in relatively good prospects in the construction and cement industry. In the Philippines, for example, cement consumption rose by 9.5% in 2009 after years of stagnation. However, even the foremost cement countries of the region, Indonesia, Malaysia, the Philippines, Thailand and Vietnam, differ greatly, each having its own particular development as regards per capita cement consumption, imports, exports, cement production capacity and utilization. This report presents the current economic data and cement figures of each country and discusses the prospects up to 2013.

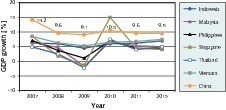

Following the global economic crisis, the ASEAN countries have become a driving force for the world economy, alongside China and India. Particularly Vietnam, Indonesia and the Philippines, who are less export-dependant than the other important countries of the region and are bolstered by a robust domestic demand, achieved a thoroughly positive economic growth in 2009 (Fig. 1). Thailand, Malaysia and Singapore were also far less severely affected by the crisis than western economies. Forecasts for 2010 and the subsequent years predict impressive economic statistics for the ASEAN...

Following the global economic crisis, the ASEAN countries have become a driving force for the world economy, alongside China and India. Particularly Vietnam, Indonesia and the Philippines, who are less export-dependant than the other important countries of the region and are bolstered by a robust domestic demand, achieved a thoroughly positive economic growth in 2009 (Fig. 1). Thailand, Malaysia and Singapore were also far less severely affected by the crisis than western economies. Forecasts for 2010 and the subsequent years predict impressive economic statistics for the ASEAN countries, which are planning to form a common market by 2015. Aside from the already named countries, ASEAN includes economically weak Myanmar, Cambodia and Laos as well as oil-rich Brunei. Altogether, the economic region has a population of about 600 million.

Many reasons have been put forward for the ASEAN countries coming through the recent global economic crisis so well. For one thing, a currency swap agreement had been concluded between the ASEAN countries and China, Japan and South Korea (ASEAN +3). Under this agreement the participating countries had formed a mutual currency reserve fund of 120 billion US$ in order to help any of them out of balance of payments difficulties and short-term liquidity problems. Although only 20% of the fund is held by ASEAN countries, the effect on stability and security from the point of view of investors is considerable. The International Monetary Fund (IMF) is losing influence in the region while that of China, already the most important trade partner before the EU, Japan and the USA, is growing.

Moreover, a trade agreement with China was signed in 2010. From the point of view of the leading ASEAN countries, the main benefits to be gained from this agreement are increased exports to China, lower production costs due to economies of scale and a growth in direct investments. All these benefits are generated by the high rate of economic growth in China. When the agreement came into force, the customs duties on 7000 commodity groups were abolished. The ASEAN countries have also concluded free-trade agreements with India (2009), Korea (2010) and Australia/New Zealand (2010), which are now being progressively implemented. However, very little progress has so far been achieved in this respect with the EU. It is therefore hardly surprising that the ASEAN countries are increasingly aligning with Asia and the EU is only playing the role of the biggest investor.

Thanks very largely to government investments and economic stimulus packages, there has been a distinct upswing on the building and construction sector and the demand for cement in ASEAN countries (Table 1). Even on an international scale, the region‘s investments of between 1.4% of GNP (Indonesia) and 15.7% (Thailand) are exceptional figures. It is, of course, true that particularly in the sector of infrastructure improvement measures the ASEAN countries still have a lot to do. The Asian Development Bank (ADB) estimated an investment requirement of 596 billion US$ or around 60 billion US$ per year for the period 2006–2015. This corresponds to approximately five times the average amount invested by the private sector in the preceding years (Fig. 2). The ADB came to the conclusion that it is particularly necessary to expand Public Private Partnership (PPP) programmes.

Among the most important infrastructure improvement programmes are the energy and transport sector (roads, railway, harbours and airports) and the water supply and sanitary network. The building and construction sector is benefitting particularly from the increasing demand for housing and business accommodation, shopping centres and touristic facilities. A recently published study by STR Global on the hotel situation in ASEAN countries showed a distinct increase in capacity utilization and earnings per room. A total of approx. 230 new hotels are under construction or in the planning stage in the five important cement countries, 80 of them in Thailand alone, 53 in Indonesia, 43 in Vietnam, 27 in the Philippines and 25 in Malaysia. The cement industry is profiting from the continuing expansion of the infrastructure and from the increasing urbanization, which is simultaneously providing the necessary economic momentum in the countries of the region.

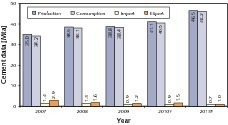

Table 1 provides an overview of the cement industry in the ASEAN countries. At the end of last year, the available cement production capacity was approx. 230 million tonnes per year (Mta). Around 150 Mta of cement was produced and also consumed. The imports of 9.1 Mta were somewhat higher than the exports. The ASEAN countries have a total of 93 integrated cement plants (excluding shaft kiln plants and mini-cement plants) and 33 pure grinding plants with capacities exceeding 0.2 Mta. The average per capita cement consumption in the region is 252 kg. However, there is a relatively large difference in range from country to country. Just in the TOP 5 cement countries the highest figures range from 544 kg (Malaysia) to 521 kg (Vietnam), while the lowest figures range from 157 kg (Philippines) to 158 kg (Indonesia). The capacity utilization figures of the plants also vary greatly between 80.5% (Indonesia) and 49.6% (Thailand).

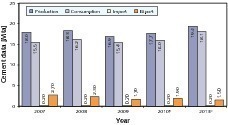

After a temporary slump in cement consumption growth in 2009, with its increase of only 0.9% to 38.4 Mta and a decline in exports, the country has returned to a positive climate for the cement industry (Fig. 3). The forecast for 2010 is a strong growth of 5.4% in cement consumption, bringing it to 40.5 Mta, so that consumption will approximately keep pace with the economic growth. Cement output is expected to rise to approx. 41.1 Mta. Up to 2013 the cement producers consider it possible that cement consumption will increase further at annual growth rates of 4.5%. If exports and imports develop as shown, cement consumption will rise to 46.2 Mta and production to 46.5 Mta. The per capita cement consumption is expected to rise from 158 kg to 180 kg. As a consequence, the overall outlook for the coming years is a rosy one. The present capacity utilization of 80.5% demands new investments.

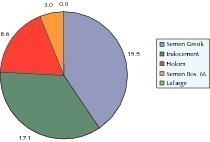

In Indonesia there are nine different cement producers who are members of four different groups (Fig. 4). Semen Gresik has a cement production capacity of 19.5 Mta and a market share of 40.5%. The company is 51% state-owned. Semen Gresik operates the PT Semen Gresik plant in East Java, PT Semen Tonasa in South Sulawesi, PT Semen Padang in West Sumatra, PT Semen Baturaja in South Sumatra and PT Semen Kupang in East Nusa Tenggara. In 2009, Semen Gresik (Fig. 5) increased its cement output by 2.9% from 16.7 Mta to 17.1 Mta. This resulted in a plant capacity utilization of 88%. In 2009, the company profited particularly from the growth in cement consumption in East Java (3.1%) and Sulawesi (15.7%). Due to the high capacity utilization, the company has decided to build two new 8,000 tpd cement production lines at the plant locations Tonasa and Tuban before 2012. In both cases, they contracted FLSmidth as the supplier.

Place 2 in the ranking is taken by Indocement Tunggal Perkasa, a member of HeidelbergCement. Indocement has a cement production capacity of 17.1 Mta at its plants Citeurop (11.9 Mta), Palimantan/Cirebon (2.6 Mta) and Tarjun (2.6 Mta, Fig. 6). In 2009, its cement output was 11.8 Mta after 12.54 Mta in 2008. The plant capacity utilization rates were between 65.5% (Citeurop) and 84.2% (Palimantan). In 2010 a new cement grinding plant will go into service at Palimantan, raising the factory‘s cement production capacity by 1.5 Mta. Holcim Indonesia is the 3rd-placed company with a cement production capacity of 8.6 Mta at two integrated plants (Fig. 7) and one grinding plant. Holcim is planning to invest more than 400 million US$ in Tuban for a new cement plant with a production capacity of 1.6 Mta. Lafarge, which ranks below PT Semen Bosowa Maros (3.0 Mta at two plants), will also return to a capacity of 1.2 Mta after their plant in Bandah Aceh (Fig. 8) is reconstructed.

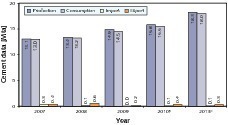

As generally expected, Malaysia suffered a slump in cement consumption in 2009 (Fig. 9). After a growth rate of 4.8% in the preceding year, cement consumption dropped by 4.9% to 15.4 Mta, so that the figures for 2007 and 2009 were practically identical. The same can also be reported for peninsular Malaysia. Here, the 2009 cement consumption dropped by as much as 6.7% after a similar increase in the preceding year. The only part of the country that registered a rise in cement consumption in 2009 was East Malaysia. Forecasts anticipate that cement consumption in Malaysia will again increase in 2010 by 3.9% reaching a level of 16 Mta. The rate of increase will rise up to 2013, but will still be lower than the rate of economic growth. Exports are expected to level out at a rate of between 1.5 and 2.0 Mta. Cement imports will remain insignificant. It is possible that the per-capita consumption could increase to over 600 kg.

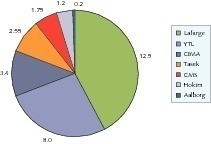

With a total of nine cement producers owned by seven different companies, the cement industry in Malaysia is relatively strongly fragmented (Fig. 10). The market leader is Lafarge Malayan Cement with a capacity of 12.5 Mta, meaning a market share of 43.7%. Lafarge owns cement factories on Langkawi, in Kanthan (Fig. 11) and Rawang, as well as a grinding plant in Pasir Gudang, on the border with Singapore. In 2009, despite a 6.7% decline in its cement markets and –10% in the case of ready-mixed concrete, Lafarge still managed to increase its pre-tax profits by 11% thanks to strict cost management. Place two in the ranking is taken by YTL Cement Berhad with a cement production capacity of 8.0 Mta (6.0 Mta clinker production capacity). In 2005, the majority of shares were taken over by PHS (Perak-Hanjoong Simen). In 2009 the company raised its turnover by 34%. In the last 10 years the company achieved a total increase in average annual turnover of 23.3%. However, this figure also includes its cement activities in China.

The subsequent rankings are occupied by the CIMA Group (Cement Industries of Malaysia Berhad) with 3.4 Mta cement production capacity and the Tasek Corporation with 2.6 Mta (2.3 Mta of clinker). Tasek owns 30% of CIS (Cement Industries Sabah), which operates a 0.9 Mta grinding plant and a cement terminal in Lahad Datu (Fig. 12). Among the smaller vendors are CMS Cement with 1.75 Mta capacity at two plants, Holcim, who operate a 1.2 Mta grinding plant, and Aalborg Cement (Cementir) who own a white cement plant with a capacity of 0.2 Mta. With the current capacity utilization of 57.1%, there is actually no basis for installing new cement production capacities. It is therefore truly astonishing that the Hong Leon Group, acting through its subsidiary Hume Cement, this year awarded Sinoma an order worth 145 million US$ for a new 5,000 tpd cement plant.

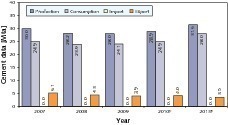

After the stagnating cement consumption figures since 2002, it is remarkable that in 2009, the year of the global crisis, the Philippines experienced a 9.5% rise in cement consumption to 14.9 Mta (Fig. 13). This effect is considered to be mainly attributable to the government‘s economic stimulus package, which led to an upswing in particularly work-intensive infrastructure projects. For 2010, a further robust increase of 7.1% is expected, bringing consumption up to 15.5 Mta. In 2013, cement consumption could be as high as 18.0 Mta, which would require average annual growth rates of 5.1%. Given the forecast population of almost 100 million, the per capita cement consumption would then be 181 kg. The amount of cement exported and imported would decline progressively. The current capacity utilization of only 54.1% also provides enough leeway for production increases in the coming years.

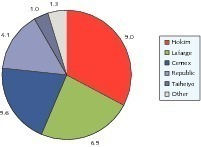

In the Philippines, there are ten cement producers that are consolidated in seven companies (Fig. 14). The market leader is Holcim Philippines with a market share of 31.5% due to a cement production capacity of 9.0 Mta. The company owns four integrated cement plants: Bulacan (Fig. 15), Davao, La Union and Lugait, as well as the grinding plant in Mabini. Lafarge is in 2nd place with a capacity of 6.5 Mta at six cement plants and one grinding plant. Acting through Republic Cement, Lafarge controls the plants Bulacan, Batangas, Teresa and Norzagaray in addition to a plant at Iligan (Fig. 16) and Mindanao Portland Cement. Republic Cement, whose member companies include FR Cement and Lloyds Richfield, have a capacity of 4.1 Mta at their own plants and their share in Lafarge plants. In the next place, Cemex has a cement production capacity of 5.6 Mta at Apo Cement and Solid Cement. The smaller companies include Taiheiyo (1.0 Mta), Northern Cement (1.0 Mta) and Pacific Cement (0.3 Mta).

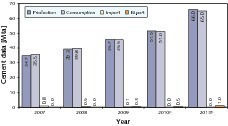

In Thailand the cement market is still not making real progress. Although cement consumption rose slightly by 0.8% in 2009, reaching 24.1 Mta (Fig. 17) and a further growth of 3.3% to a figure of 24.9 Mta is forecast for 2010, a comparison of the 2007 and 2010 figures shows that the market is stagnating. The reasons certainly include the recent demonstrations by the political opposition, which at times paralysed the capital city and sections of the economy. Higher cement consumption growth rates of 4% are only expected after 2010 and the anticipated consumption in 2013 is 28 Mta. In the medium term the country is not expected to return to the 1997 level of over 36 Mta. It is considered possible that the per-capita cement consumption could rise from the present 355 kg to 405 kg. Thailand’s exports are expected to settle at a rate of between 3.5 and 4.0 Mta. Imports will remain insignificant.

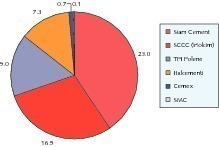

With a total of only six cement producers in the country, market shares are easy to summarize (Fig. 18). The leading company with a cement production capacity of 23 Mta or a market share of 40.8% is the Siam Cement Group (SCG, Fig. 19) with plants in Kaeng Khoi, Ta Luang, Thong Song, Lampang and Kampot. In view of the stagnation in Thailand, the company is seriously thinking of increasing its investments abroad. Its first factory in Cambodia, the Kampot cement plant went into operation in 2008. Second place in the ranking is taken by Siam City Cement Public Company (SCCC), a member of the Holcim Group, with a cement production capacity of 16.5 Mta at its Saraburi plant (Fig. 20). SCCC has placed great importance on using alternative fuels and on recuperating process heat. In 2010, waste heat recovery systems were put into operation at both the company‘s largest kiln lines.

In the subsequent rankings with two-digit market shares are TPI Polene with a cement production capacity of 9.0 Mta and Italcementi, with its 5.0 Mta Asia Cement plant (Fig. 21) in Tambon Pukrang and 2.3 Mta Jalaprathan Cement plant. Companies in Thailand with smaller cement production capacities are Cemex, with 1.2 Mta in Saraburi and Samakkee Cement (SMC), which is owned by the MK Real Estate Company, with 0.1 Mta. The total clinker production capacity of all Thailand‘s plants is 46.8 Mta, while the total cement production capacity is 56.6 Mta. Under the present circumstances and given a plant capacity utilization of 49.6%, no further growth in cement production capacity is in sight.

According to the VNCA (Vietnam National Cement Association) the cement market in Vietnam developed better in 2009 than had been anticipated in our market report [1] a few months ago. The VNCA states a 14.3% cement consumption increase to 45.5 Mta for 2009 (Fig. 22). A decisive impetus was provided by the economic stimulus package introduced by the Vietnamese government. Based on the above figure, the per capita cement consumption (PCC) is a remarkable 521 kg. Expert opinions differ regarding the prospects for a further increase. If cement consumption increases further by 12.1% in 2010, resulting in a consumption figure of 51 Mta, the PCC figure would be 578 kg. If the expected average growth rate of 8.4% up to 2013 is achieved, the cement consumption would then be 65 Mta and the PCC would be 717 kg. Considering that the present rate of urbanization is just 28%, this would be a very high figure. Vietnam is going to make the development from a net importing country to a cement exporting country.

The country already has more than 33 integrated cement plants (excluding shaft kiln plants) and 17 separate grinding plants, giving it a total cement production capacity of 61 Mta. State-owned Vicem has a capacity of 21 Mta (Fig. 23) and a market share of 34% [1]. A particularly large market growth is currently being enjoyed by a number of private companies such as Vinaconex (Fig. 24). Given this scenario, the present production capacity of 61 Mta will rise by a further 45 Mta up to 2013 if all the planned projects are implemented according to the plan. 41 Mta of the existing capacity is already located in the northern part of Vietnam, while a further 20 Mta are at plants in the south of the country. Due to the local raw material deposits, orders for the construction of new plants in the north are still being awarded. The latest example in Thanh Hoa province is the 11,000 tpd plant of Cong Thanh Cement, which is being constructed by Polysius.

The problem regarding surplus capacity and transportation of cement in Vietnam has already been comprehensively discussed [1]. In the meantime, the Ministry of Building and Construction has ordered the regional and provincial governments not to permit any further cement projects [2]. Nevertheless, if existing cement projects are implemented on schedule, no justification can be seen for the assumed surplus capacity of about 20 Mta in 2013 (105 Mta capacity at 80% utilization = 84 Mta output at 65 Mta demand). It is not clear how much cement Vietnam can export or how competitive the country‘s cement will be on the Asian and world markets. Moreover, what amount of old capacity (shaft kiln plants and other uneconomical factories) can be shut down and what degree of capacity utilization will be needed for economical plant operation and for the repayment of credits?

At the moment, the cement industry in ASEAN countries has good growth prospects, particularly in Vietnam, Indonesia and the Philippines, i.e. mainly in those countries with a relatively low rate of urbanization and a comparatively low per capita cement consumption. In contrast, countries whose per-capita consumption is already relatively high, such as Malaysia and Thailand, will only experience a limited growth. However, in addition to the already stated parameters the expansion of infrastructure, the future population growth rate and the per-capita income play a not insignificant role in future scenarios. In Indonesia, for example, a strong increase in the middle class is forecast, which will boost the demand for high-quality living accommodation. Also decisive for an increasing demand for cement is the availability of reasonably priced cement and other building materials, as well as affordable credit for housing purchases.

Überschrift Bezahlschranke (EN)

tab ZKG KOMBI EN

This is a trial offer for programming testing only. It does not entitle you to a valid subscription and is intended purely for testing purposes. Please do not follow this process.

This is a trial offer for programming testing only. It does not entitle you to a valid subscription and is intended purely for testing purposes. Please do not follow this process.

tab ZKG KOMBI Study test

This is a trial offer for programming testing only. It does not entitle you to a valid subscription and is intended purely for testing purposes. Please do not follow this process.

This is a trial offer for programming testing only. It does not entitle you to a valid subscription and is intended purely for testing purposes. Please do not follow this process.