Ethiopia’s cement industry is booming*

![1 Distribution of Ethiopia‘s gross national product [1]](https://www.zkg-online.info/imgs/101525493_fda43c1e91.jpg)

Summary: Although Ethiopia is one of the poorest countries in the world, it is currently experiencing a two-digit economic growth. An essential factor in this economic upswing is the construction sector, a fact that also greatly benefits the country’s cement industry. In Ethiopia the available capacities are far too small to meet the increasing demand for cement. More than 1/3 of the present cement consumption is therefore imported, which has driven cement prices up to very high levels. Against this background, a gigantic expansion of cement production capacity is currently taking place. The question is: how much cement will the country actually need in the coming years?

With its 82 million inhabitants, Ethiopia has the second largest population in Africa after Nigeria. In recent years, the country has achieved an astonishing two-digit annual economic growth. In spite of the worldwide economic crisis, it still experienced a growth of 9.9 % in 2009, after 11.2 % and 11.8 % in the preceding years. This places Ethiopia at the forefront of economic growth in Africa and also gives it a leading ranking in an international context. However, it must not be forgotten that its per-capita income of about US$ 350 makes Ethiopia one of the poorest...

With its 82 million inhabitants, Ethiopia has the second largest population in Africa after Nigeria. In recent years, the country has achieved an astonishing two-digit annual economic growth. In spite of the worldwide economic crisis, it still experienced a growth of 9.9 % in 2009, after 11.2 % and 11.8 % in the preceding years. This places Ethiopia at the forefront of economic growth in Africa and also gives it a leading ranking in an international context. However, it must not be forgotten that its per-capita income of about US$ 350 makes Ethiopia one of the poorest countries in the world. On the basis of HDI-1 (Human Poverty Index) the country is among those lagging behind. Ethiopia is therefore one of the countries that receives a large amount of international aid. In addition to the traditionally strong development cooperation with Germany and other Western European countries, as well as the USA and Japan, a great deal of financial aid has been received from China and several Middle Eastern countries in recent years. This is partly due to the country’s strategic location on the Horn of Africa.

The most well-known of Ethiopia’s export commodities is coffee. However, coffee exports have been decreasing over recent years, so that they now make up little more than a quarter of the country’s exports, after accounting for over 50 % of the exports in the 1990s. In the meantime oilseed exports have taken a quarter share of exports, while the stimulant drug Kath and flowers each account for 9 –10 %, ranking ahead of exports of leather and leather products, gold and pulses. All in all, the agricultural economy has become less important for the country‘s gross national product (GNP) (Fig. 1), even though it can be supposed that around 3/4 of all workers are primarily engaged in agriculture and livestock farming. As a result of the high two-digit growth rates of recent years, the service sector has taken over from agriculture as the most important economic factor. In the course of this trend, particularly high growth rates have been achieved in the sectors of finance, hotels/restaurants, trade, real estate, the educational sector and public health.

In contrast, the share of the industrial sector in the country’s GNP has stagnated at 13 %. However, the government is currently making intensified efforts to strengthen this sector. One of the declared aims is to expand the energy economy by constructing further hydroelectric power stations and thus to end the country’s chronic shortage of electrical energy. Furthermore, it is intended to build up an ethanol production industry to reduce Ethiopia’s dependence on oil imports. The leather and textile industries are already being developed and their export figures reflect the initial successes on these fields. The metal industry and the engineering sector are to be further expanded in order to reduce the country’s dependence on foreign goods and to bolster the development of processing industries with domestic products. The resultant reduction in imports of spare parts and components will lead to considerable foreign exchange savings.

Ethiopia’s construction industry is profiting primarily from the housing boom, followed by infrastructure projects such as the improvement of the road network, expansion of the water supply/irrigation system and development of power supply facilities. According to the EIA (Ethiopian Investment Agency), 8851 investment projects were approved in Ethiopia during the fiscal year 2008/2009. 826 of these were construction projects with a financial volume of 81 billion Ethiopian Birr (ETB) (5.9 billion US$). 654 (79 %) of the construction projects, or approx. 96 % of all investments, with a value of ETB 78.4bn, are to be implemented in Addis Ababa [1]. With its 3.2 million inhabitants, the city houses just under 4 % of the country‘s population. Consequently, extensive building sites are currently dominating the urban landscape of Addis (Fig. 2). The city authorities are planning to construct 80 000 new housing units per year in order to overcome the lack of living accommodation. A tremendous boom in hotel and office construction is also obvious.

On the other hand, the greater portion of Ethiopia is of a rural nature (Fig. 3). Urbanization has so far only reached a level of 16 %. This is reflected in the road network. In 1997 the average distance of members of the population to asphalted roads was 21 km and in 2009 it was still almost 12 km. In the intervening 12 years the road network had been extended from 25 000 km to 46 800 km, requiring an investment of more than 600 billion ETB, over 51 % of which had come from the national budget. But even today, there are only about 6900 km of asphalted roads, although 90 % of these are now in a good condition after only 17 % in 1997. Ethiopia currently only has an installed power station capacity of approx. 1600 MW, 90 % of which is generated by hydropower. However, the country’s hydroelectric generation potential is around 45 000 MW. The government plans to expand electricity generation capacity to 8000 MW in the next 5 years and to 16 000 MW in 10 years [2]. This development plan places particular emphasis on regenerative energy sources.

The government, which was returned to office by an overwhelming majority in the May 2010 elections, intends to maintain the two-digit growth rate. The national budget will be raised by approx. 20 % in 2010/11. Infrastructure development is to remain one of the most important objectives. Restricting inflation to below 10 % is also being afforded highest priority. Almost 47 % of the entire budget is earmarked for development projects, including 888 million US$ for road construction alone. The rest is mainly intended for expansion of electricity generation facilities and the power network, the water supply system and irrigation measures, as well as improvement of the public health system.

In recent years, cement has become a rare commodity in Ethiopia. The retail price for 1 Quintal of cement (= 100 kg) was up to 350 Birr (250 US$/t) in June 2010, which makes the cement market very attractive for investors, but is delaying a large number of construction projects. However, it should be noted that the ex-works price of the two largest cement producers Mugher Cement and Messebo Cement is between 140 and 180 US$/t, depending on the type of cement. 60 % of the cement sold by these two companies is used in government projects, while the remainder almost completely goes to contractors. Traditionally, only two types of cement are produced, approx. 20 % being Ordinary Portland Cement (OPC) and 80 % being Portland Pozzolana Cement (PPC). OPC is marketed as OPC 42.5 PPC and PPC as PPC 32.5, with 20 –30 % pumice being employed as intergrinding material. The country has sufficient raw material deposits (Fig. 4) to last for a very long time.

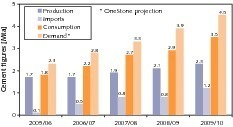

Ethiopia’s cement industry stagnated until 2006/07 (Fig. 5), with cement production figures of approx. 1.7 million tonnes per year (Mta). Cement factories were and still are unable to utilize their full cement production capacity because of limited power availability and, in some cases, because of poor condition of the equipment. Meanwhile, the country’s cement output has been increased to 2.3 Mta with a number of new plants. The difference between the cement production and consumption figures is imported. Ethiopia does not export cement. Initially, imports were less than 0.2 Mta but in the meantime they have climbed to over 1.2 Mta. This means that over 1/3 of the cement consumption is imported. The major portion of the imports comes from the Middle East and Pakistan via the harbour of Djibouti. Annual cement demand has always been significantly higher than the actual cement consumption, with this gap increasing over the years.

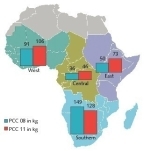

From 2005/06 up to today the per capita cement consumption figure of 25 kg has risen to approx. 43 kg (Fig. 6). On an international scale, but also compared to the rest of Africa, where the average per capita consumption figure is 156 kg, Ethiopia brings up the rear. There is no point in comparing Ethiopia with North African countries, which have an average per-capita consumption of over 500 kg. This is largely due to the fact that all North African countries have a significantly higher degree of urbanization. For instance, in Libya, the country with the highest per-capita cement consumption, the degree of urbanization is 77 %. The sub-Saharan countries have an average per-capita consumption of 82 kg [3]. Even the other countries of East Africa, like Sudan, Kenya or Tanzania with their figures of 91, 86 and 47 kg, are ahead of Ethiopia. If cement demand is taken as a yardstick, the per-capita cement consumption would be 55 kg.

Table 1 presents an overview of existing cement factories and producers. At present, the production capacity of the total of 10 factories is 2.64 Mta. 8 factories are integrated cement plants while 2 are just grinding plants. All the small capacities of up to 0.09 Mta are shaft kiln plants or mini cement plants. Up to now, 9 cement producers are represented in the market. Alongside local companies, investors from China and Pakistan are also active. The top international cement producers have so far not become involved in the Ethiopian market. The companies that have been present longest in the Ethiopian market are Mugher Cement, Messebo Cement and National (Dire Dawa) Cement.

Mugher Cement currently operates two plants and has a cement production capacity of approx. 0.9 Mta. The factory at Mugher was built in 1985 by ZAB Dessau. It consists of two parallel kiln lines with a capacity of 2 x 1000 t/d (Fig. 7). The company also owns a grinding plant in Addis Ababa, whose kiln line was shut down in 1992. Since a leasing contract for the grinding plant was concluded with Avorniga, clinker from abroad has also been ground there. A new 3000 t/d clinker production line is currently under construction (Fig. 8). The contractor is Sinoma, although critical components such as the raw mill, the grate cooler, packer etc. have been ordered from Germany. The clinker will be ground in a new grinding plant in Tatek, 10 km west of Addis (split grinding). The factory is located in the vicinity of a pumice deposit. Pumice is a typical component of PPC cement manufactured in Ethiopia. Mugher Cement has announced plans to build a 10 000 t/d production plant after the factory currently under construction has been completed.

Messebo Cement operates a relatively new cement factory with a capacity of 0.85 Mta and a 2,000 tpd kiln line (Fig. 9) supplied by FLSmidth in the north of the country. The latter plant was brought on line in 2000/01. The kiln system includes a five-stage preheater with inline calciner. Raw material and cement grinding are performed by ball mills. For coal grinding a Loesche vertical mill was later installed. A new 1.4 Mta plant is currently under construction (Fig. 10). The contractor is CNBM and the associated HCRDI (Hefei Cement Institute). The new plant will be equipped with a modern kiln line including precalciner. For raw material grinding a vertical roller mill by Loesche is used. Construction of this facility is stated to be mainly on schedule, although completion is not planned before January/February 2011.

National Cement looks back on the longest history of all Ethiopian cement producers. Its first cement factory with a clinker output of 120 tpd was built in Dire Dawa in 1938. National Cement resulted from the privatization of a former state-owned operation and the later takeover of 80 % of Dire Dawa Cement stock by East African Holdings. In October 2007 the plant was upgraded with the aid of Chinese technology to a clinker output of 500 tpd or 0.15 Mta cement production capacity (Fig. 11). At present, Mertec Services is carrying out a further upgrade of the core plant components (Fig. 12). National Cement contracted the Chinese company SHMG, a member of the Northern Heavy Industries Group, to construct a new cement plant (Fig. 13) at a distance of 3 km from the existing factory. Commissioning of the new plant, which will have a clinker output of 3000 tpd and a cement production capacity of 1.2 Mta, is scheduled for 2011.

Apart from the established cement producers, a number of newcomers have entered the Ethiopian market. Derba Midroc, owned by Midroc Holding, is one of the most interesting new companies. The reason for this is definitely not the two existing shaft kiln plants owned by the company, but rather the new construction of a production line for 5000 tpd of clinker or 7000 tpd of cement near the village of Derba, about 75 km

north of Addis. Three other companies that operate shaft kiln plants and mini cement plants are among the newcomers to the market. These include Abyssinia Cement (Fig. 14) and Debresina Business Industries (Fig. 15). Chinese companies like Huang Shan Cement, who have up to now only imported clinker, and Red Fox, who own a grinding plant, are now interested in the cement production market.

In the last few years, the Ministry for Trade and Industry (MoTI) have issued 33 licenses for cement projects. It cannot necessarily be assumed that all of these projects will actually be implemented. Individual projects concern plant capacities of up to 7.8 Mta, and also include the possibility of exporting cement. As Ethiopia has no harbour of its own and the transport distances are relatively long, the competitiveness and sense of such projects is questionable. Table 2 shows those projects that could possibly already be ready for operation in 2010 and 2011 and also presents a list of interesting projects that may be realized at later dates.

The data show that, if everything goes according to plan,

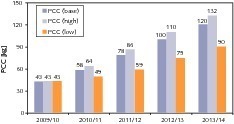

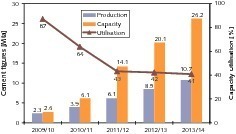

3.5 Mta of new cement production capacity may already be ready for operation in 2010. In 2011 a further 8.0 Mta may then follow. While the projects in the period up to 2009 provided a relatively small amount of new capacity, the current projects – except for a few exceptions in 2010 – are already plants of international standard. Probably the most important of these is Derba Midroc’s 7000 tpd cement plant (Fig. 16) that is currently under construction. Judging from the already existing capacity, it is conceivable that cement production capacity could increase about tenfold by 2013/14, reaching a figure of approx. 26.2 Mta (Fig. 17). If all the projects are actually implemented, a capacity of 32 Mta is also possible by 2013/14. Their implementation depends decisively on whether the investors’ currently optimistic attitude can be maintained over the coming years and on the development of cement sales.

On the basis of the cement demand of 4.5 Mta in 2009/10, an increase to 4.9 Mta in 2010/11 would appear possible if cement prices are suited to market requirements. This would represent a rise of 40 % compared to the actual cement consumption in 2009/10. A similar increase in the following year is also conceivable (Fig. 18) and cement consumption could increase with somewhat reduced growth rates to 11.0 Mta by 2013/14. Such an increase would surpass the achievements of practically every other country. Given the described basis scenario, Ethiopia’s per capita cement consumption would rise from 43 kg to 120 kg (Fig. 19). A realistic expectation, covered by the high and low scenario, would be a range from 90 kg to over 130 kg. In Ethiopia, some people have highly ambitious expectations for a per capita cement consumption of up to 350 kg by 2015.

The scenarios concerning the future development of cement consumption and cement production capacity are highly uncertain. The reasons for this are that the increase in cement consumption has been relatively slow in recent years, which was largely due to the fact that the market was very inadequately served. Due to this unsatisfactory data basis, forecasts of the future cement consumption and per capita cement consumption remain speculative. However, the data for the future expansion of the country’s cement production capacity are more concrete. The forecast increases in consumption and capacity result in the expected production capacity utilization (Fig. 20). This shows that a great reduction in capacity utilization is certain, which will result in reduced profitability due to non-utilized plant capacities. Up to now, absolutely no shutdowns of existing cement production lines are planned. Furthermore, it is still probable that imports will be higher than exports.

Überschrift Bezahlschranke (EN)

tab ZKG KOMBI EN

This is a trial offer for programming testing only. It does not entitle you to a valid subscription and is intended purely for testing purposes. Please do not follow this process.

This is a trial offer for programming testing only. It does not entitle you to a valid subscription and is intended purely for testing purposes. Please do not follow this process.

tab ZKG KOMBI Study test

This is a trial offer for programming testing only. It does not entitle you to a valid subscription and is intended purely for testing purposes. Please do not follow this process.

This is a trial offer for programming testing only. It does not entitle you to a valid subscription and is intended purely for testing purposes. Please do not follow this process.