The cement industry in 2013 with substantial changes

Summary: The cement producers are expecting to emerge stronger from the current economic crisis. However, the fact is that the preconditions for the companies vary widely and that, as in sport, there are losers as well as winners. On the other hand, the forecasts in the business reports of even the leading cement companies contain only relatively vague predictions. To create a well-founded database on this subject the OneStone Consulting Group has carried out a new market study to make a thorough analysis of the world cement market covering over 100 cement-producing countries [1]. The current cement consumption figures for 2009 are used, the imports and exports are highlighted and the further development of cement production capacity figures and capacity utilization figures is examined. The way the market potential will unfold in the future is very important for plant suppliers.

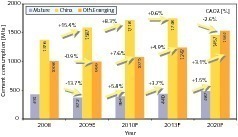

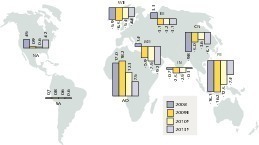

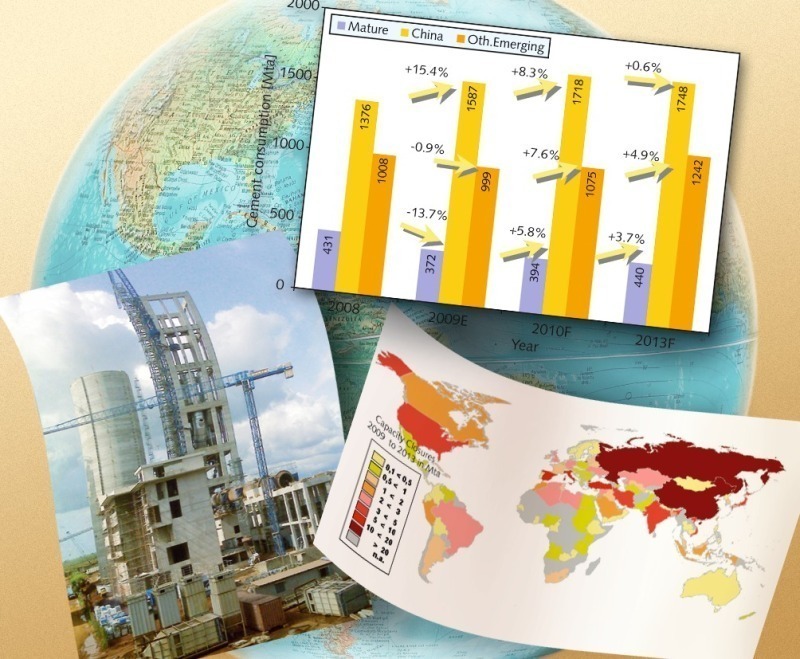

A collapse in world cement consumption was widely feared, but in fact the new market study shows worldwide consumption figures for 2009 of 2960 million t/a after 2815 million t/a in 2008, which corresponds to a growth of 5.1 %. However, Figure 1 shows that without China there were major losses. In the “mature” markets the consumption fell by 13.7 % or 59 million t/a. In the other emerging markets apart from China the losses were only 0.9 % or 9 million t/a. The diagram also shows how cement consumption will probably change up to 2020. A significant...

A collapse in world cement consumption was widely feared, but in fact the new market study shows worldwide consumption figures for 2009 of 2960 million t/a after 2815 million t/a in 2008, which corresponds to a growth of 5.1 %. However, Figure 1 shows that without China there were major losses. In the “mature” markets the consumption fell by 13.7 % or 59 million t/a. In the other emerging markets apart from China the losses were only 0.9 % or 9 million t/a. The diagram also shows how cement consumption will probably change up to 2020. A significant recovery of the losses in the markets apart from China will already be discernable in 2010, but the growth in China will weaken.

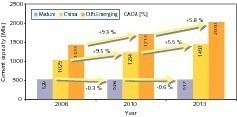

The forecast for 2013 gives a worldwide compound annual growth rate (CAGR) of 4 % based on the figures for 2008, and there will be a steady decrease in the share taken by China in the next few years due to the saturation of the market there. From 2013 it is expected that cement consumption in China will fall annually by as much as 2.6 % by 2020. In contrast, the outlook in the other markets is very positive; the growth in the other emerging markets will be relatively high with 4.9 % up to 2013 and 3.1 % after 2013. Even the former mature markets will achieve sustainable growth rates again of 3.7 % and 1.5 % respectively. However, it must be remembered that although these good figures represent a recovery after the sharp collapse in 2008/2009

the markets in the individual countries will vary widely.

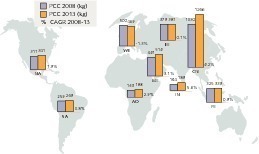

The past and future per capita consumption figures (PCC in kg) form the basis for predicting the cement consumption figures in the market study. On the one hand, the relationships between gross national product, economic growth and PCC are relatively well known and on the other hand there are some relatively accurate assessments of the future economic growth (International Monetary Fund) and of future population growth (Population Reference Bureau). One result of these analyses from the market study is shown in Figure 2. This shows how the PCC will change from 2008 to 2013 for the nine regions being examined. The only region with negative growth is Western Europe. The largest percentage growths will occur in India, China, the Middle East and Africa/Oceania. From this it is already possible to deduce various consequences for the cement industry.

and in worldwide trade

The change in price from 2008 to 2009 was largely non-uniform across the countries. The reduced demand led to significant collapses in price in only a few countries, notably in the Commonwealth of Independent States, in some western European countries and, for example, in Pakistan (Fig. 3), but the prices in North America were largely maintained in spite of a serious drop in sales. On the other hand, the cement prices rose in large areas of South America, in the Far East and Africa. China is an exception in that significant drops in price had to be accepted in spite of a massive growth in sales. The general worldwide price level has also increased. In a great many countries the price of standard cement (OPC) ex works is over 120 US$/t. The reasons for this are, among others, the heavy demand and increased production costs in which particularly high energy costs have had an effect.

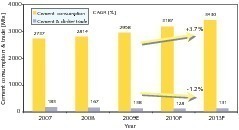

The worldwide trade in cement and clinker had already declined in the years from 2007 to 2008 [2, 3]. The reasons for this were essentially the growth in production capacity in many former cement-importing countries, but also the reduced consumption in some countries that occurred largely at the expense of imports. There was an increasing drop in the ratio of trade to cement production (Fig. 4). A further decrease in the trade of cement and clinker by 1.2 % is expected from 2009 to 2013. A slight increase again in 2013 is possible. It is expected that the trade in clinker will increase while the trade in cement will decrease. One region for which this is particularly applicable is Africa, or sub-Saharan Africa [4]. Other regions/countries with a slight recovery will be North America/USA and Western and Eastern Europe.

When the possible import and export volumes of cement are examined for the different regions it is apparent that from 2008 to 2013 the calculated export figures stand in an increasingly unfavourable ratio to the import figures (Fig. 5). The gap between assumed imports and exports will become ever larger. In 2008 this was still around 5.5 million t/a, but in 2009 there was an increase to 19 million t/a. This means that in some countries there was increasing stockpiling of clinker in 2009 in the hope that there would be a rapid improvement in sales conditions. However, the problem will tend to be intensified in 2010 through additional production capacity, with the result that a sales gap of 21 million t/a is expected. A drop in the surplus capacity to 18 million t/a is not predicted until 2013.

New cement-making capacity has risen faster than cement sales in recent years. This trend will continue over the next few years. Figure 6 shows the trend for mature markets, China and other emerging markets; the figures do not take account of any cement from shaft kiln plants. The production capacity in mature markets will fall but there will be a significant increase in the rest of the world. The annual growth rates in the other emerging markets will be larger than the growth rates for cement consumption. This means that these countries will be faced with losses in capacity utilization or with closing down uneconomic plants and kiln lines. China will not be affected directly by this problem as about 600 million t/a of old capacity are to be closed down anyway.

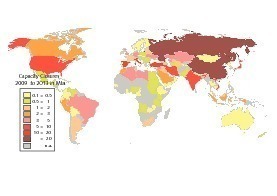

From the market analysis and Figure 6 it is clear that about 1200 million t/a new cement production capacity will be ready for operation by 2013. China will account for about 425 million t/a of this, the other emerging countries for 740 million t/a and the mature markets for only 40 million t/a. This is contrasted with anticipated closures (without China) of 52 million t/a in the mature markets and 140 million t/a in the other emerging countries. Figure 7 indicates where the major closures will take place around the world. In addition to China it is mainly the Commonwealth of Independent States that are affected, as well as Western Europe and other countries in Eastern Europe, countries in North Africa, the Middle East, India, some countries in the Far East and in North and South America. The closures will primarily involve obsolete kiln plants that would in any case be replaced by new facilities for economic reasons. However, some cost-effective plants will also be affected by new, large, modern lines.

For Western Europe there continues to be the problem of the relatively high cost of clinker and cement production, which may be intensified by the problems of CO2 and the efforts by Europe to lead the way in its reduction. In the medium term the importation of clinker will definitely increase. On the other

hand there is already some overcapacity, as has become very clear during the last year. The sustainability of the production facilities in these markets will ultimately only be secured by modern environmental technology (Fig. 8). Wherever cost-effective clinker production is impossible there will be conversions to grinding plants or full works closures. As a whole, there is no doubt that the producers will only be able to achieve acceptable results in the markets by adjusting their production capacities.

A great deal of new production capacity has been built in the Middle East in the last three years (Fig. 9). In this region there is still about 170 million t/a new production capacity under construction or at the planning stage. Many projects only ma-terialized through local capital and very high expectations for the future cement requirements and possible export rates. Cement projects are often a purely local matter. An important part is apparently played by the fact that investors are sometimes faced by few options and preference in investment calculations is given to prospects of rapid payback. For example, there have been individual cases where investors have decided to build a cement plant solely on the basis of overseeing/participation in individual construction projects, such as airports, dams or resorts, on the assumption that there would be the option of exports in the future.

4 Development of the market potential

for plant and machinery suppliers

Contracts for 425 million t/a new clinker capacity were placed from 2006 to 2009. This does not include China or cancelled projects. Up to 2008 the plant manufacturers experienced a real boom in orders, sometimes with greatly extended delivery times [5]. Figure 10 shows the great drop in the orders from over 120 million t/a to about 40 million t/a in 2009. There has been a significant shift in the market shares of the plant manufacturers. The Chinese plant manufacturers Sinoma and CNBM have become serious competitors for established companies such as FLSmidth, Polysius and KHD. This is even more astonishing because Sinoma and CNBM have their own large cement-making facilities in China and are competitors to the international companies there, namely Lafarge, Holcim and HeidelbergCement. However, in other countries these companies award contracts to what are effectively their competitors.

The growing influence of the Chinese companies in the market is significant not only in the contracts awarded for clinker-producing facilities but now also in almost all the individual product groups within a cement plant. The study shows, for example, how the market shares of the established suppliers and of the Chinese suppliers have changed in recent years. The fact that Chinese plants with virtually exclusively Chinese technology are being built in certain regions, especially in countries in Africa and Asia such as Vietnam or Ethiopia, is often underestimated. However, there are also still some product groups where Chinese suppliers have only a small share of the market outside China. These include e.g. vertical mills, palletizers and on-line analyzers.

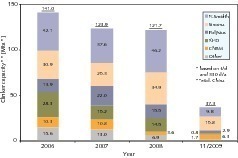

According to project lists there will still be almost 600 projects throughout the world (without China) lined up by 2013 for extending clinker- and cement-producing facilities with a total of about 800 million t/a of new cement-making capacity. In the market study a check was made on the projects for contracts that have already been awarded. This shows that from 2010 to 2012 contracts will be awarded for about 230 million t/a new clinker capacity with an increase from year to year. From this it can be deduced that the market potential for mechanical equipment will fall from about 7.7 billion US$ in 2008 to 4.15 billion US$ in 2010 and 5.0 billion US$ in 2013. Taken as a whole this is still a good outlook for the plant manufacturers after the boom years from 2006 to 2008. However, the competition will sharpen significantly. In all probability no discounts or large price reductions will be given for machines and plant, and the customers will at best profit from shorter delivery times.

The market study shows in great detail the fundamental changes that will take place in the cement industry by 2013. For reasons of space only a few aspects can be examined in this review. Because of the recovery in many difficult cement markets in 2010 and good sales growth in many emerging markets the investment climate will improve significantly and projects that have been stopped will resume again in a few months. However, the market picture will be clouded by the poor prospects for cement exports. The fact that apparently a minority of investors tend to look beyond individual national markets and regions will be an advantage for the prospects in cement plant construction. In spite of the market potential in plant manufacture, which may be considered by many to be unexpectedly high, there will be tightening of international competition.

Überschrift Bezahlschranke (EN)

tab ZKG KOMBI EN

This is a trial offer for programming testing only. It does not entitle you to a valid subscription and is intended purely for testing purposes. Please do not follow this process.

This is a trial offer for programming testing only. It does not entitle you to a valid subscription and is intended purely for testing purposes. Please do not follow this process.

tab ZKG KOMBI Study test

This is a trial offer for programming testing only. It does not entitle you to a valid subscription and is intended purely for testing purposes. Please do not follow this process.

This is a trial offer for programming testing only. It does not entitle you to a valid subscription and is intended purely for testing purposes. Please do not follow this process.