Feasibility of sustainability scenarios

Source/Quelle: WBCSD, ECRA

Source/Quelle: WBCSD, ECRA

Source/Quelle: www.cemfocus.com

Source/Quelle: www.cemfocus.com

Source/Quelle: www.cemfocus.com

Source/Quelle: www.cemfocus.com

Source/Quelle: www.cemfocus.com

Source/Quelle: www.cemfocus.com

Source/Quelle: UNIDO/GNR Database

Source/Quelle: UNIDO/GNR Database

Source/Quelle: WBCSD, ECRA, OneStone

Source/Quelle: WBCSD, ECRA, OneStone

Source/Quelle: Vecoplan

Source/Quelle: Vecoplan

Source/Quelle: Holcim

Source/Quelle: Holcim

Source/Quelle: WBCSD, ECRA, OneStone

Source/Quelle: WBCSD, ECRA, OneStone

Source/Quelle: WBCSD

Source/Quelle: WBCSD

Source/Quelle: www.cemfocus.com

Source/Quelle: www.cemfocus.com

Source/Quelle: IEA

Source/Quelle: IEA

Source/Quelle: HeidelbergCement

Source/Quelle: HeidelbergCement

Source/Quelle: ECRA

Source/Quelle: ECRA

Source/Quelle: ECRA

Source/Quelle: ECRA

Source/Quelle: Lafarge

Source/Quelle: Lafarge

The cement industry is currently considering scenarios for the period up to 2050, particularly with regard to the subjects of CO2 and sustainability. What are the good points of these scenarios and what ought to be reviewed or corrected? This article provides an overview.*

1 Introduction

1 Introduction

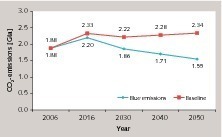

As a general point, it should be noted that the Blue Emissions variant is in line with the climate policy objective of limiting global warming to 2–3 °C. In order to achieve this CO2 reduction from 2.34 Gt to 1.55 Gt, the WBCSD/IEA regards four reduction measures to be necessary. The two bodies consider that so-called Carbon Capture and Storage (CCS) methods would account for the greater reduction of 56 %, while conventional methods would in total only achieve a minority reduction of 44 %. Under conventional methods, alternative fuels would provide a 24 % reduction, while higher efficiencies and a lower clinker factor would each bring 10 %. Based on the emission level of 1.55 Gt in 2050 compared to 1.88 Gt in 2006, the stated measures should, according to the roadmap, reduce the CO2 output of the cement industry by 17.6 %. However, the CO2 emission would rise further to 2.2 Gt up to 2016 and the CCS technologies would only have a substantial effect as from 2030.

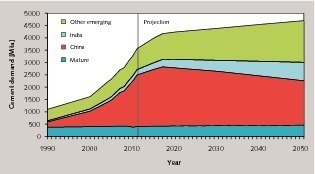

Naturally, the CO2 emissions of the cement industry not only depend on the implemented reduction measures but also on the actual production level. Contrary to the moderate projections of up to 4400 Mta, other forecasts predict significantly higher figures: for example the IDDRI (Institut de Développement Durable et des Relations Internationales), expects 5000 Mta in 2050 and a study by WWF/Lafarge predicts 5500 Mta [2]. Of course, the production volume has implications for the CO2 reduction measures. A higher volume means that a far greater amount of alternative fuel or clinker substitute has to be obtained. It is unclear what consequences larger production volumes would have on the age of cement plants and thus on their energy efficiency. In the case of CCS, numerous plants would have to be equipped with the technology. This raises the question of whether the planned investments would be sufficient and where the finances for the higher expenses should come from. Ultimately, the ratios of the individual CO2 reduction measures will very probably shift away from those envisaged in an assessment by Mott MacDonald [3].

2 OneStone market outlook

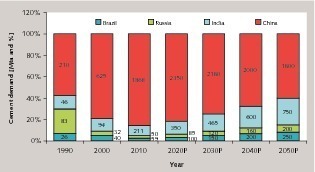

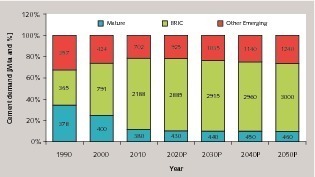

The ratios of the BRIC countries Brazil, Russia, India and China will alter. China’s share will substantially decline between 2016/17 and 2050 to 60 %, while India’s share of 9.6 % (2010) will increase to 25.0 % (2050) (Fig. 3). It is expected that India’s production volume in 2050 will be 750 Mta. In 1990, Russia’s figure of 83 Mta represented a share of 22.7 %, which slumped to 2.3 % by 2010. In 2050 Russia will be producing around 200 Mta, which means a share of 6.7 % in the BRIC countries’ figures. Brazil will overtake Russia and will be producing about 250 Mta of cement by 2050. Figure 4 shows the situation again for the mature (developed) and emerging countries. This shows the great influence of the BRIC countries, which will, however, lose a few percentage points from 66.9 % in 2010 to 63.8 % in 2050. The winners are the other emerging nations, who will increase their share from 21.5 % to 26.4 %.

3 Feasibility of the WBCSD/IEA projections

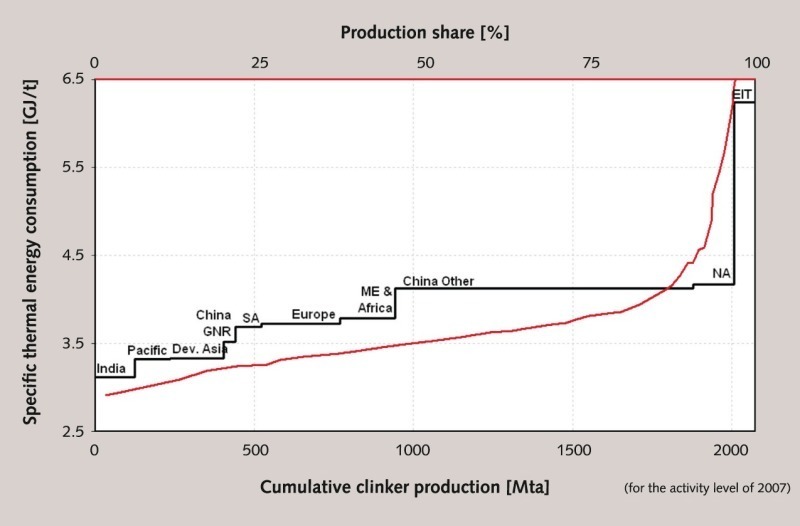

The WBCSD/IEA projection assumes on the basis of the ECRA Technology Papers that the average thermal energy consumption of 3.7 GJ/t clinker (Europe, 2006) can be reduced to 3.3-3.4 GJ/t clinker by 2030 and to 3.2-3.3 GJ/t clinker by 2050. However, the actual global figures are still significantly higher than these figures (Fig. 5). Lower figures are only achieved by plants in India and other Asian countries. The newest and best clinker production lines in China achieve 3.5 GJ/t clinker. Other Chinese plants have consumption figures of 4.1-4.2 GJ/t clinker. Plants in North America and in the CIS countries have significantly worse figures because of the still large number of wet-process kilns. By 2030 the wet kilns will certainly have been completely replaced by new modern plants. However, the plants with large capacities that have recently been built in China – and these have a total capacity of over 1000 Mta – will not yet have been replaced by 2030.

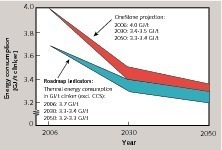

One factor preventing a further improvement of the specific heat consumption is the still high usage rate of alternative fuels, which raise the energy consumption by around 0.3 GJ/t clinker because of their lower average calorific value and the heat losses of the required bypass system. The increasing application of WHR systems also has a general tendency to increase the specific heat consumption, particularly if the configuration includes additional firing systems. If CCS systems should come into widespread use after 2025, this would also significantly subtract from possible improvements in the specific heat consumption. OneStone Research forecasts (Fig. 6), that – on the basis of the current average figure of 4.0 GJ/t clinker – the best figures achievable by 2030 will be 3.4 to 3.5 GJ/t clinker, and by 2050 the best case scenario will be average figures of 3.3 to 3.4 GJ/t clinker. This means that the CO2 emission reduction due to the reduced energy consumption will be 7 % (10 % WBCSD/IEA projection).

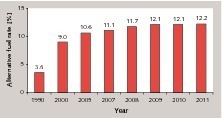

Proceeding from today’s situation, it will be necessary to make far greater efforts if the ambitious targets for 2030 and 2050, requiring a CO2 emission reduction by the factor of 3 to 7, are to be achieved [6]. Fig. 8 indicates how difficult the realization of these aims is likely to be. It shows the development of the alternative fuel rate for Holcim, one of the leading companies on this sector. With a rising usage rate of alternative fuels, the incremental increase progressively declines. This saturation effect is partly a consequence of problems with obtaining and processing the fuels, but is also due to the fact that an increasing alternative fuel usage rate results in a significant increase in equipment and handling costs [6]. At present, Holcim achieves a biomass rate of 25 % in its alternative fuels. In the developed countries it will be difficult to improve on this rate.

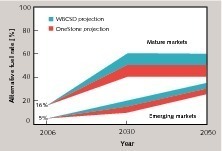

OneStone Research considers that the scenarios for alternative fuels are too optimistic. In the developed countries the positive results hitherto achieved in, for instance, Northern Europe cannot be projected onto Southern Europe. Instead of an alternative fuel rate of 40-60 % in the developed countries in 2030 and 2050, only 40-50 % is considered possible (Fig. 9). The rate of biomass is forecast to be not higher than 30 %. In the emerging countries, an alternative fuel rate of 10-15 % is considered possible for 2030, while 20-30 % may be achieved by 2050. These figures depend especially on the extent to which alternative fuels can be organized and utilized in the BRIC countries. However, in any event it is unlikely that those countries would achieve biomass rates in excess of 30 %. Correspondingly, the attainable CO2 emission reductions due to the usage of alternative fuels will be 15 % (24 % WBCSD/IEA projection).

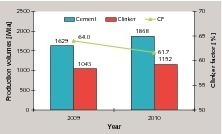

Figure 11 shows market data for China based on the cement and clinker production figures published by the China Cement Association (CCA) and the China Building Materials Academy (CBMA). According to these, 1868 Mta of cement and 1152 Mta of clinker were produced in 2010, for example. These figures result in a clinker factor of 61.7 % for 2010 after e.g. 64 % for 2009, if one calculates from the figures of the previous year. These figures may seem unrealistic, but they reflect the Chinese efforts to produce cement in the most cost-effective manner possible. Given China’s current global market share of 57.1 % and the estimated clinker factor of 79 % in the rest of the world, the present global clinker factor is already below 70 %, or to be precise, 69.1 %. This scenario indicates that it should be possible to even achieve a clinker factor of 60 % in 2050. The CO2 emission reductions due to the reduced clinker factor will be 26 % (10 % WBCSD/IEA projection).

4 CCS, oxyfuel and post combustion technologies

The cement industry has been occupied with this subject for around 10 years now. The pioneering companies include HeidelbergCement and Cemex. HeidelbergCement plans to commission its first demonstration system supplied by Alstom or Aker Clean Carbon (ACC) at the Brevik plant (Fig. 13) of Norcem by 2013/14. Cemex plans to install a demonstration system in the USA with financial support from the US Department of Energy (DOE). This system will use technology supplied by RTI International. The technological bases exist at the equipment suppliers and also at the ECRA (European CementResearch Academy), which has been very intensively engaged in the development of this technology for some years now and has published various reports on the subject [8-10]. Such university institutes as the Technical University of Hamburg-Harburg are also working in this field.

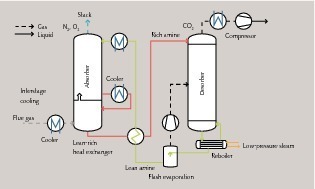

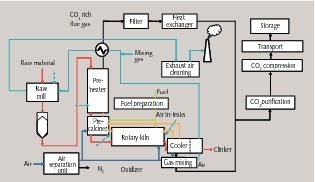

Three main CCS technologies are offered: post-combustion, pre-combustion and oxyfuel processes. Pre-combustion processes are not applicable in the cement industry. Post-combustion processes apply a chemical absorption method. According to the ECRA, no CCS systems have yet been put into operation in the cement industry. Figure 14 illustrates the design principle of an absorption system, in which e.g. ammonia is used as the solvent. For comparison, Figure 15 shows an oxyfuel process that includes an air separation unit and needs pure oxygen to be used in the cement manufacturing process instead of air. While an absorption process affects the clinker production process only slightly or not at all, an oxyfuel process involves the issue of changed CO2 partial pressure behaviour in the production process, for which hardly any research data is available. Moreover, it can be expected to affect the burning characteristics or cause changes in the burning zones in the kiln. Up to now, there are no findings indicating a significant effect on the cement properties [11].

There are several different estimates regarding the additional expenses involved in CCS processes. The IEA’s Cement Technology Roadmap 2009 predicts extra costs of 475-590 billion US$ up to 2050 for CCS technologies, depending on whether the low or high variant of the Blue scenario is followed. ECRA predicts that an oxyfuel process alternative would cost around 330‑360 million € up to 2030, and then 270-295 million € per plant up to 2050 because of technology cost reductions. The operating expenses of such a system are reckoned to be 8-10 €/t clinker. As a consequence, clinker production costs would increase by around 40 % and the additional costs for every tonne of CO2 avoided would be around 33-36 €/t [12]. This would make plants equipped with CCS uncompetitive compared to conventional cement plants.

5 Prospects

Überschrift Bezahlschranke (EN)

tab ZKG KOMBI EN

This is a trial offer for programming testing only. It does not entitle you to a valid subscription and is intended purely for testing purposes. Please do not follow this process.

This is a trial offer for programming testing only. It does not entitle you to a valid subscription and is intended purely for testing purposes. Please do not follow this process.

tab ZKG KOMBI Study test

This is a trial offer for programming testing only. It does not entitle you to a valid subscription and is intended purely for testing purposes. Please do not follow this process.

This is a trial offer for programming testing only. It does not entitle you to a valid subscription and is intended purely for testing purposes. Please do not follow this process.